An article written by the Investment Migration Council Editorial Team for the IM Yearbook 2023

While it is impossible to predict the future, it is possible to consider how current megatrends and potential future disruptions might affect investment migration in the years to come. We look at the global shifts reshaping the world and ask what are the implications for investment migration?

- Welcome to the metaverse

The idea of virtual citizenship isn’t new. In fact, it has been debated ever since Linden Lab launched its online platform Second Life in 2003. At its peak, Second Life reported millions of active users in self-made virtual worlds complete with property sales, a market of virtual goods, and a functioning economy that was worth around US$500 million in GDP around 2007, according to Time magazine.

While Second Life might not represent the broader vision of the modern metaverse, it can certainly be called a metaverse pioneer. Interest in the metaverse spiked in recent months amid a rise in sales of non-fungible tokens (NFTs) as well as investment from big tech companies in the space. In fact, the metaverse has become a mainstream topic since the day Facebook changed its name to Meta in October 2021.

But what exactly is the metaverse? The word itself means “beyond the universe”. One way to describe it is the convergence of digital and physical lives, making the metaverse a space where you can interact with virtual objects in real life and with real-time information. Philip Rosedale, Founder of Second Life, told the World Economic Forum in 2022: “The most important meaning of ‘metaverse’ is the mission to make the internet a live experience with other people always there, as opposed to the largely individual experience it is today.”

Bloomberg Intelligence expects the market opportunity for the metaverse to reach US$800 billion by 2024. According to a report published by Citi Research, the metaverse represents a potential trillion to US$13 trillion opportunity by 2030, that could boast as many as five billion users. Likewise, Goldman Sachs arrived at a US$12.5 trillion opportunity if one-third of the digital economy shifts into virtual worlds and then expands by 25%. “We believe the metaverse is the next generation of the internet — combining the physical and digital world in a persistent and immersive manner — and not purely a virtual reality world,” their report reads.

More importantly in an investment migration context, KPMG predicts that by 2040 the concept of digital citizenship is thriving, and many people have done away with their passports and residency cards for the physical world. The consulting firm further forecasts: “There are at least 11 virtual nations now with a combined population of 200 million ‘citizens’ and a GDP above US$100 billion each. Their citizens enjoy higher incomes and live in ‘gated communities’ that have their own security. Benefits like virtual welfare, employment, and other amenities are vastly superior to those provided by physical nations, creating a substantial lifestyle gap between citizens of physical nations and those in virtual nations, who are dual citizens of the physical country they reside in.”

The future of the metaverse is far from certain, and many say the metaverse is still several years away. However, a likely scenario is that individuals are physical residents of one country but meta citizens of another because they connect with the values, ideologies, and laws of the meta state more than with those of their base in the real world. Moreover, they conduct business with like-minded forward-thinkers in the metaverse, attend the best universities online, and invest in digital real estate using crypto.

It’s time to start thinking about the metaverse because some of investment migration’s selling points and experiences are fast becoming metaverse elements. Much like the entertainment industry must decide if it is sticking to a shrinking market for traditional forms of amusement, or start bringing their characters and brands into metaverse platforms, the big question for investment migration is: how can it capitalise on the metaverse? Now is the time to experiment and invest and innovate in metaverse-based use cases.

2. Cryptocurrencies and investment migration – a match made in heaven?

Cryptocurrencies hit a rough patch in 2022. Since November 2021, the crypto market has dropped 60% – drastically falling from a market cap of $3 trillion to less than $1 trillion in October 2022. The collapse of Sam Bankman-Fried’s FTX exchange in November 2022 served as just another example of the unpredictable nature of the industry. However, the onset of the so-called crypto winter as this period of market cooling has become known is one reason why cryptos are playing an increasingly important role in investment migration.

Given the volatility of the market, many crypto millionaires are diversifying part of their net worth into other hard assets such as real estate. Both agents and pathways report that they have seen a surge in enquires from those who have made a fortune from cryptocurrency investments, as well as from those who want to invest in digital currencies and are looking for a crypto-friendly base.

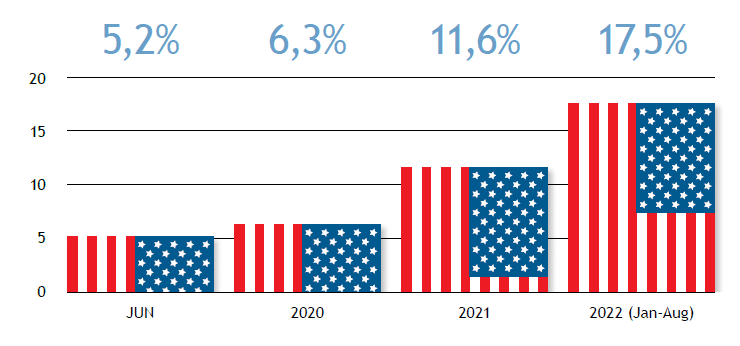

In the past few years crypto assets have moved from being niche products to having a more mainstream presence. In June 2021, the UK Financial Conduct Authority published its fourth consumer research publication on crypto-assets ownership, which found heightened public interest in, and media coverage of, cryptos, with 78% of adults now having heard of cryptocurrencies. Around 2.3 million now own crypto assets, up from around 1.9 million in 2020.

In the US, Pew Research, a nonpartisan think tank in Washington, reported that 16% of survey participants indicated they had personally invested in, traded or otherwise used cryptocurrencies. Elsewhere, Newsweek Magazine cited a survey from January 2022 by crypto firm New York Digital Investment Group, estimating the total number of Americans who own cryptos at 46 million, which is about 14% of the population.

It comes as no surprise that the investment immigration industry is gearing up to the use of cryptos. Portugal, which is generally regarded a crypto hub, and St. Kitts and Nevis, as well as Antigua and Barbuda have emerged as the leading investment migration countries with crypto-friendly policies. One key advantage of cryptocurrencies is they do not rely on intermediaries such as commercial banks and credit card companies to conduct transactions, which cuts out the inefficiencies and added costs of these intermediaries. In the Caribbean, it also addresses correspondent banking issues that have long plagued the region. Portugal is accepting bitcoin and other cryptocurrencies for real estate investment in its golden visa programme. While the country had been notable for having no crypto taxes on individuals, in October 2022 the government proposed to impose a 28% income tax on cryptocurrencies held for less than a one-year period. Meanwhile, Antigua and Barbuda, as well as St, Kitts and Nevis are members of the Eastern Caribbean Currency Union, which developed its own digital currency called DCash. While it remains to be seen if DCash will elicit the same level of enthusiasm as bitcoin and other cryptocurrencies, it is another example that shows that crypto assets as well as its associated products and services have grown rapidly in recent years and are here to stay.

3. Sustainability: True impact or green washing?

The world is more than ever under pressure to channel money into curbing climate change – and yet fighting climate change seems to have slipped down on many nations’ agenda as the Ukraine war, high energy prices and geopolitical tensions took precedence in 2022.

The hardest work is still to come. The reality is that not enough has been done in the last 12 months – some would argue we have moved backwards,” Hortense Bioy, Global Director of Sustainability Research at Morningstar, told Reuters in November 2022.

Moreover, sustainable investing has come in for a great deal of criticism since the turn of the year with the list of companies and countries that have been accused of not being as ESG- friendly as promoted getting longer by the day. Case in point: Human rights advocates pointed out concerns about Egypt’s human rights record ahead of Cop27, the UN climate summit that took place in the Egyptian resort town of Sharm el-Sheikh in November 2022.

In 2020, the Investment Migration Council highlighted that investment migration has the potential to advance the 2030 Sustainable Development Agenda (SDG). Investment migration brings in fresh capital, human skills, and entrepreneurial capacity for the receiving nation. Some of this money contributes, often unintendedly, towards meeting the SDGs.

For example, investment migration income made important contributions to the funding of physical and social infrastructure, particularly to finance the reconstruction of infrastructure damaged by hurricanes that have hit the Caribbean. Elsewhere, investments migration is directed to business investment that create jobs and therefore reduces poverty.

However, to ensure that investment migration income is not overlooked as a factor within a country’s overall sustainability and development strategy, countries should apply ESG criteria to investment which form part of an investment migration pathway. There is a strong need for a more streamlined and systematic approach and to better integrate ESG factors so that investment migration can positively impact the world.

4. Are you ready for the next generation of clients?

Generation Alpha, the children of Millennials born between 2010 and 2024, promises to play a key role in shaping our society within the next couple of decades and is expected to be the generation with the largest spending power yet. While, for the time being, investment migration is largely driven by Gen X and Millennials customers, we ask what are some of the typical traits we can expect from the next generations?

Generation Z, those between 1995 and 2009, are the first digital natives. They have grown up with smartphones and tablets and since an early age had internet access at home. They consume mainly digital media and are used to watch a video summarising an issue rather than read an article covering the topic. Due to social media platforms such as Facebook and Instagram, Gen Zs are constantly connected to and influenced by their peers. Moreover, Gen Zs tend to be highly educated, environmentally conscious and longing to leave a positive impact within communities.

The 2022 edition of the Wealth report predicts that between 2021 to 2026 the global UHNWI population will grow by a further 28%, more than a doubling in numbers over a 10-year period. This growth will consist mainly of Millennials and Gen Zs as they inherit assets and companies from their parents or else as innovators and successful start-up owners particularly in the technology field.

Generation Alpha, or Gen Alpha, is the demographic cohort succeeding Generation Z and is made up of mostly the children of Millennials. The name derives from the first letter of the Greek alphabet. Mark McCrindle, a demographer who rose to fame for analysing and naming generations, says members of Gen Alpha are the first generation to have been born and fully shaped in the 21st century. They are also expected to be the largest generation ever. By 2025, they will number two billion globally and most of them will live in Asia – mainly in China and India.

By 2030, the first members of Gen Alpha will be young adults, and they are the next generation of customers that will benefit from the largest intergenerational wealth transfer in history. Much like Gen Zs, Gen alpha will be digital. They are growing up in a world where TikTok, Roblox and Instagram are not disruptors but the established incumbents, McCrindle emphasizes.

While sustainability is already important to Millennials and Gen Z consumers, it is expected that Gen Alpha will resonate especially strongly with sustainability, given that they will be growing up entirely under the threat of climate change. There is also consensus among researchers that Covid-19 will have a lasting impact on this cohort since their formative years have been shaped by a global pandemic. So, it’s perhaps unsurprising that many believe that Gen Alpha can be defined by their worries towards becoming ill and not being able to see their families for a long period.

Although the demographic transition is still a few years away, the investment migration community needs to start catering for these new realities. For Gen Z and Gen Alpha themes such as the environment, general wellbeing, and technology ought to be more central, while those who wish to win them as clients need to adapt their communication methods. Bureaucracy, antiquated portals and slow processes will not attract the upcoming generations. What started with Gen Z will continue with Gen Alpha. Those born after 2010, McCrindle summarises, will be more digital, global, social and visual than any generation before them.

5. The new reality: remote working and nomad visas

Estonia gave rise to successful companies like Skype, Wise, Bolt and Playtech, and it was the first country to launch a digital nomad visa in 2020, which fast became the ultimate concept for countries to attract remote workers. Just two years later, in 2022, more than 25 countries run similar programmes, according to a Migration Policy Institute report, making it one of the most important trends in the immigration space in recent years.

Sparked by the pandemic, remote work has become an integrated part of today’s work fabric. Even as companies such as Uber and Tesla try to reign in personnel back to their brick-and-mortar offices, there is consensus that remote work will remain mainstream and an important tool for companies to recruit and retain employees.

Concurrently, freelancing is on the rise. In 2021, according to the US Bureau of Labour Statistics, over 47 million Americans voluntary quit their jobs and trends predict that by 2027 50% of the workforce will be freelancing in the country.

While people’s reasons for quitting their jobs vary, of course, the inclination is that those with a high level of education and in possession of sought-after specialised skills, are opting for flexible projects with several companies instead of a stable contract with a single business. This trend has reduced the need of one to be permanently based in one location to be close to his/her place of work or business. Instead, tech-savvy individuals are moving to far flung exotic nations to strike a better work-life balance, explore new places without the need of taking a career break and, at the same time, escape crowded cities.

This has markedly created a new niche for countries to cater for this increased demand of individuals wanting to work remotely from outside their home country. What has been termed as a ‘digital nomad visa’ is fundamentally a programme that gives an individual the legal right to work remotely while residing away from their country of permanent residence. Some programmes have been specifically designed for remote workers while others have been adapted from earlier work visas.

While some variations exist among them, they generally follow the same idea: granting a temporary hassle-free residency permit that allows foreigners to stay from six months to five years. The onset of these programmes addressed a legal vacuum for remote workers wanting to spend an extended period abroad working independently, although there are still some unanswered questions about tax liability.

Applying for a digital nomad visa generally involves an application fee together with proof of a certain level of income to sustain oneself. The fees vary from being at no cost when applying for a visa in Georgia to US$2,000 for the Barbados ‘Welcome Stamp’ programme.

Income requirements range from US$1,275 per month under Ecuador’s visa programme to US$100,000 per year under the Cayman Islands ‘Global Citizen Concierge Programme’. Average rates hover around €3,000 per month as per Malta’s ‘Nomad Residency Permit’, and the Cypriot, Panama, and Romanian nomad visa programmes.

With an estimated 35 million digital nomads worldwide contributing to a global economic value of US$787 billion per year, it’s no surprise that countries around the world are launching their own digital nomad visa programmes. This new visa trend has generally been positively received by local communities and has spurred several developments. Co-working and co-living spaces have boomed, and in some places, entire areas have been built to cater for the influx of these new communities.

The concept of digital nomad visas is only a few years old and essentially still an experiment. However, judging from the increasing number of countries coming up with their own programmes and the growing number of digital nomads worldwide, it’s likely that digital nomad visas are here to stay.

6. Start-ups going global

For centuries, some of the biggest companies in the US have been founded by immigrants – just think of Levi Strauss from Germany or Elon Musk from South Africa. An analysis by the National Foundation for American Policy from May 2022 found that immigrants have started more than half of America’s start-up companies valued at US$1 billion or more. Attracting a start-up before it grows big can have a huge impact on a country’s economy. For instance, Berlin-based fashion e-commerce company Zalando grew to become the 10th biggest employer in the city over the last 12 years. While it’s incredibly difficult for smaller countries to attract investment from established companies such as Google, chances are they will succeed in attracting the founders of the ‘next Google’ to start up in their location. This is the rationale driving the rapid expansion of start-up visa programmes.

In 2022, around 40 nations, including most OECD countries, had some form of start-up-related programme in place. In fact, migration policies in many countries are moving away from being focused on traditional family or employment-related immigration and crafted more around entrepreneurial and highly skilled individuals. This ‘merit based’ approach is proving popular. A growing global nationalistic environment driven mainly by populist ideologies is not leaving much space for the ‘traditional’ immigration policies.

Start-up related visas attract fewer negative sentiments, do not generally spur contentious opinions, and garner wider partisan support. Secondly, if managed properly, start-up visa programmes can potentially leave substantial economic multiplier outcomes on a nation’s economy creating growth opportunities in new innovative areas. Contrary to entrepreneur-related visas which have been around for a while, start-up visa programmes focus on the potential of a business, rather than the actual capital invested. The main goal is that of augmenting the national start-up ecosystem by attracting talent and ideas from abroad. Differences exist between various programmes, including whether they offer temporary or permanent status, how they are assessed and monitored, the sectors targeted, and the investment requirements and commitments. In most cases only temporary renewable residence permits are offered.

Canada is one of a handful of countries that through its Start-up Visa (SUV) programme offers permanent residency to successful applicants. Most programmes offer family members temporary residency with working rights. Japan and Korea conversely do not admit family members via their start-up programmes.

There is no single method on how start- up programmes are evaluated and selected. Unlike other immigration programmes based on investment, net worth or skill set, most start-up visas are about enticing and supporting business owners before they succeed and leave a positive impact on the local community. Start-ups are in essence high risk with many failing after few years operating. Managing the associated risks is key for these programmes.

A balance needs to be struck between venturing on a great entrepreneurial potential but mitigating the associated risks through selection, monitoring and support structures. Most governments involve players from the local business community and expert panels to assist and guide immigration personnel who do not possess the ability to assess promising business plans. Lithuania for example has a panel of experts, the majority of which come from the private sector assessing applications. The UK involves universities, while Finland, the Netherlands, and Malta allot their innovation and business agencies to select applications. Some programmes, such as those offered in Poland, France and Spain even offer some limited form of capital assistance via grants and business incubators.

Attracting the right start-ups from around the globe can reap tangible economic benefits for countries. Replicating the Silicon Valley success story is an end target for many programmes. Apart from job creation, successful start-ups sustain and spread a culture of innovation and entrepreneurship. They can also boost the marque of countries, both regionally and globally. For instance, entrepreneurs who have followed Chile’s ‘Start up Chile’ programme over the last decade or so have generated sales of more than one billion dollars worldwide. Chile, which was a pioneer in devising international start-up programmes more than ten years ago, has become a hub for start-ups in Latam attracting in the process international highly skilled talent.

Start-up visas are by design low-volume. A well planned and successful start-up visa programme needs to be supplemented by wider policies such as incubators, business networking avenues and tangible investment incentives. With more countries coming up with start-up related visa programmes, having the right ecosystem is what will differentiate one programme from the other. If successful, a start-up visa programme can enhance a country’s standing on the global scene, create new high growth sectors, attract talent, and assert a government’s commitment to entrepreneurship and innovation.